Would you like to know where the money in a business goes? Are you looking at getting into a career in a stable and growing field? Do you like a start to finish process? If any of these questions have piqued your interest, this brief introduction to accounting will be a valuable resource for you. Whether you have 20 minutes to read through the essentials, or 3 hours to follow the links, you will walk away with helpful information to pursue an accounting degree as well as an overview of the topic.

Table of Contents

Section 1: Accounting Cycle

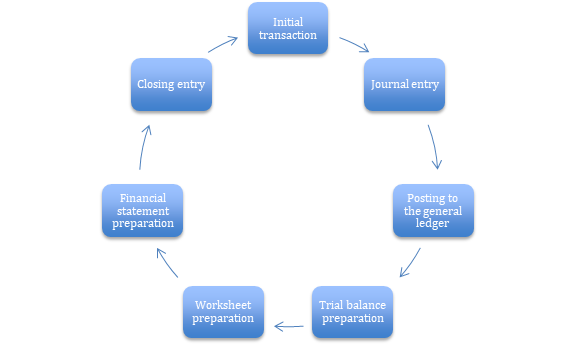

The accounting cycle is one of the most important processes in the entire world of accounting. From the first transaction to the final closing of the account, it sums up the entire accounting process. Company accounts are kept up and continued through this process to ensure payments are handled. The cycle acts as the accountability for all money to be known and balanced. Although there are different approaches, the main steps in the cycle are as follows:

- Initial transaction

- Journal entry

- Posting to the general ledger

- Trial balance preparation

- Worksheet preparation

- Financial statement preparation

- Closing entry

What do you think?

Which general ledgers are you familiar with?

Which steps in the accounting cycle require the most time and thought?

Additional Resources for the Accounting Cycle

Section 2: Main Accounting Principles

The following concepts are referred to as the Generally Accepted Accounting Principles, also known as GAAP. They’re set by the Financial Accounting Standards Board.

- Accrual principle: States that transactions should be recorded when they occur rather than when the payment was received.

- Conservatism principle: States that expenses and liabilities should be recorded immediately, while revenues and assets should only be recorded when they occur.

- Consistency principle: States that once you start using a specific method of accounting, you should stick with it until you find something inherently better.

- Cost principle: States all businesses should only record assets and liabilities at their original cost.

- Economic entity principle: States a business owner’s personal transactions should never mingle with the transactions of their business.

- Full disclosure principle: States you should offer all necessary information required for the reader to understand a financial statement in plain sight, printed on the statement.

- Going concern principle: States that you should assume your business will continue to operate into the foreseeable future.

- Matching principle: States that all expenses should be recorded alongside revenue.

- Materiality principle: States you should record any transaction which may have the chance of influencing a future decision for anyone reading a financial statement.

- Monetary unit principle: States that only transactions that can be measured in common currencies should be recorded.

- Reliability principle: States that it’s only necessary to record transactions that can be proven.

- Revenue recognition principle: States that revenue should only be determined as such after the earnings process is completed.

- Time period principle: States that businesses should stick to a standard time in which to report their earnings and transactions.

What do you think?

Which accounting principle do you find most intriguing? Why?

Additional Resources for Main Accounting Principles

Section 3: Financial Accounting and Business Management

The daily operations of every business are completely dependent on money: If a business’s finances aren’t in order, the entire company will face immediate and detrimental consequences. The role of accounting and finance in business management is huge, and all accountants must understand how the two fields overlap.

An understanding of how financial accounting and business management interact will allow accountants to:

- Create financial records that will allow management and shareholders to understand the company’s place in the industry

- Determine the company’s place in the industry relative to the competition

- Develop plans and strategies that will make it possible for the company to excel

- Analyze both short- and long-term operations to decide what’s working and what isn’t

- Create budgets in a responsible, sustainable manner

A thorough grasp of how finance and business management interact will allow accountants to better serve their employers. It will also give them the skills necessary to operate their own business if they choose to open one someday.

What do you think?

What role do you see business management play in accounting?

Additional Resources for Financial Accounting and Business Management

Section 4: Functions of Accounting

Accounting is a broad field with many areas of specialty, and accountants fulfill several different functions in a business.

Here are the main functions that accountants can fulfill for a business:

- Internal auditing: Accountants who specialize in internal auditing work to minimize fraud and mismanagement within the business. They ensure that a business’s finances are being handled properly, and make sure that no employees are abusing their position or stealing from the company. This reduces the company’s losses while also building confidence for shareholders.

- Management accounting: Management accountants work closely with the management team of a business to boost profits and extend the company’s reach. They may analyze competitors so they can help managers set the prices of goods and services more effectively.

- Financial accounting: Financial accountants focus on recording all transactions and creating financial statements for a business. These statements can be shared with investors and other people on the outside who have a stake in the business.

- Tax accounting: Tax accountants have the important task of making sure that all tax regulations are followed by a business. They work closely with the management team to file tax returns to save as much money as possible for the business.

What do you think?

Which function of accounting would you most like to fulfill?

Additional Resources for Functions of Accounting

Section 5: Taxes

The Internal Revenue Code (also known as the IRS) sets strict guidelines that govern all United States businesses. Tax accountants must learn to navigate these laws and thoroughly understand how they apply to all United States businesses. Every business in the country must comply with tax laws, whether it employs one single person or ten thousand.

Tax accounting is one of the most in-demand accounting specialties, and some accountants focus entirely on this very complex area. Different businesses are subject to different laws, and tax accountants must learn how to work with them all. They learn all the penalties a business or individual will face if they don’t comply with tax laws, as well as how to avoid them. To gain a complete understanding of the field, tax accountants also must understand why these laws were put in place to begin with.

The entire field of tax accounting centers around tracking funds and ensuring the IRS receives their share of the profits. Students focus on tax accounting basics during their undergraduate accounting program, but there are so many different regulations that it takes years of detailed study to learn them all. This is the reason that many accountants choose to pursue a master’s degree in tax accounting.

Subspecialties of tax law include:

- Federal income tax law

- Individual income tax

- Business income tax

- State and local taxes

- Financial planning and taxes

- Calculating gains and losses

- Property tax

- Corporations and partnerships

What do you think?

Is tax accounting a specialty you are considering?

Additional Resources for Taxes

Section 6: Bookkeeping

What is bookkeeping in accounting? Bookkeepers are critical for every business. There’s always a need for detail-oriented, critically thinking individuals to record transactions and prepare financial statements. Intuit QuickBooks is the preferred bookkeeping tool for many established businesses. This software makes it easy for accountants to process payroll and track other work-related expenses of the company. Bookkeepers will track debits and credits. Precise bookkeeping will allow the company to know where they stand with their finances. It also provides financial information to investors, the government and other external users.

Some general bookkeeping concepts are:

- General ledger preparation: a summary of a company’s transactions including credits and debits

- Financial statements: preparing balance sheets and income statements

- Payroll: paying wages and reporting taxes

- Merchandise inventory: recording costs and reporting inventory of a business’ merchandise

- Fraud prevention: prevention techniques for theft and embezzlement

What do you think?

Which part of the bookkeeping process is most interesting to you?

Additional Resources for Bookkeeping

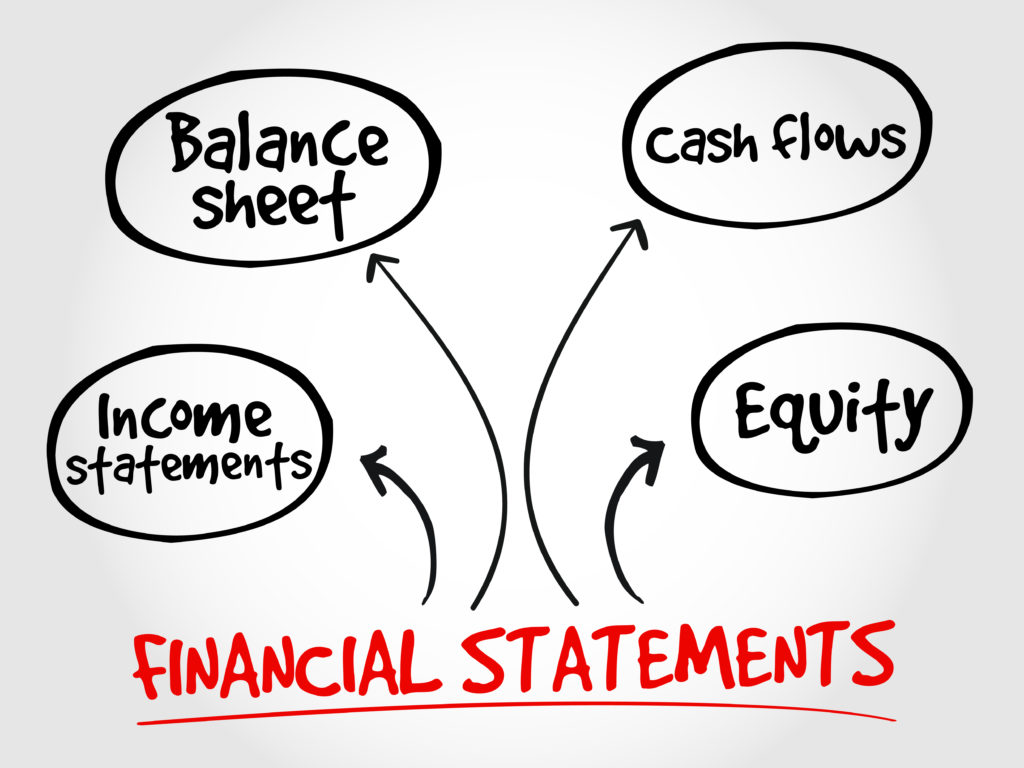

Section 7: Financial Statements

Keeping detailed financial statements is a key skill for every accounting major, and all accounting programs stress the importance of recording daily transactions. Accountants must become familiar with the process of writing financial statements and learn how the different types of statements relate to each other.

The definitions of the three main financial statements are as follows:

- Income statements: Displays a company’s revenues and expenses during a specific period. It’s sometimes called a “profit and loss statement” as well.

- Cash flow statements: Shows the amount of cash that enters and leaves a company during a given period.

- Balance sheets: A versatile report that displays assets, equity, and liabilities for a company. It also allows accountants to calculate the rate of return. It can show how much money shareholders have invested, as well as how much money is owed to and by the company.

Detailed knowledge of these three key statements allows accountants to effectively analyze financial data from competitors. They can also use these statements to gauge their company’s overall performance and determine how to improve its ranking in the industry. Mastering the creation and analysis of these three statements allows accountants to compile annual reports and determine a company’s overall health as well.

What do you think?

How familiar are you with the financial statement process?

Additional Resources for Financial Statements

Section 8: Technology and Accounting

In recent years, technology has had a major impact on accounting and how financial transactions are processed. From the most popular bookkeeping programs to state-of-the-art tax technology, the latest programs have been designed to make an accountant’s job easier.

Those in the accounting field must stay current on emerging technology and learn how to use it to their advantage. Excel and QuickBooks are general ledger programs taught in most college-level accounting courses. Some classes will prepare students to pass a certification exam such as the MOS Excel test upon completion of the program. These basic computer programs are essential for nearly all common accountant job duties, such as:

- Payroll

- Report preparation

- Competitor analysis

- Tax preparation

Recent accounting technology to watch for:

- Cloud Computing- Online storage of data is already a familiar concept to many. Forbes reports that the public cloud storage market will increase to $331.2B by 2022. The ease of storing, saving and retrieving information makes Cloud computing ideal for accountants. These programs will require a subscription. QuickBooks offers an Online version. Other programs include Kashoo, Xero and FreshBooks. For Futher Study: Cloud Computing Tutorial for Beginners (YouTube)

- Blockchain Technology- This database secures transaction information with all involved parties and allows it all to be stored in the same place and efficiently accessed. For Further Study: Block Geeks Video Guide: What is Blockchain Technology

- Automated Accounting Technology- Data-entry is becoming a thing of the past. Automated technology is the way forward and may find those with an accounting background reinventing their role within a company. For Further Study: Accounting, Automation and Change (YouTube)

- Optical Character Recognition (OCR)- This software scans documents and translates them into machine-recognizable text. This includes hand-written notes, receipts, and photos. The OCR software can search through these saved items that allow accountants easy access to these materials. For Future Study: Computerphile Optical Character Recognition (OCR)

What do you think?

How do you see technology transforming accounting?

Section 9: Accounting Key Facts and Terms

Types of Accounting Jobs

Accountants are indispensable to the success of a business. There are many specialties an accountant may choose to pursue.

Some of the most common accounting careers are:

- Certified Public Accountant (CPA): CPAs must pass the Uniform Certified Public Accountant Examination to earn their certification. CPAs are in high demand as business consultants for a wide variety of industries. They’re qualified to take on many different accounting roles, from tax preparation to finance management.

- Tax Accountant: Tax accountants must be highly familiar with all state and federal tax laws. They prepare taxes for both businesses and individuals and can choose to work for a business or on a freelance basis. They also offer guidance on how to strategize to receive the largest income tax refund.

- Chief Financial Officer (CFO): Many medium-to-large businesses employ a CFO to oversee the entire financial department. The CFO works closely with the CEO and the rest of the accounting staff to create detailed budgets and financial plans. They also handle report preparation and shareholder relations.

- Staff Accountant: Staff accountants are one of the most common accounting professionals, and there’s bound to be a few students in every class who aspire for this position. They handle bookkeeping and report preparation, as well as budget creation. This entry-level position will often be an accounting major’s first step after graduation.

Additional Resources for Accounting Jobs

Basic Accounting Terms

- Accrual: Adjustments such as expenses and losses that have been completed but not paid. Accruals may impact a company’s net income, even though money has not yet been exchanged.

- Cost: The cash required to purchase any type of asset, including transportation fees.

- Expenses: The costs required for a company to operate and make money. Wages and cost of inventory are two examples.

- Revenue: The total income a company receives from all business processes.

- Income: The total amount earned after deducting all expenses and costs from the revenue.

- Loss: Incurred whenever a company loses money.

- Capital: All financial assets held by a company.

- Fund: Money set aside for a specific reason, such as insurance or charitable foundations.

- Gain: Money earned after selling an asset.

- Investment: A monetary asset purchased in the present that is intended to appreciate over time.

- Liability: Money owed to another individual or company.

- Net profit: Calculated by subtracting the cost of goods sold from the total sale price.

Accountant General Job Duties

What are good entry-level accounting jobs? To answer this question, it’s important to first understand an accountant’s general job duties.

Entry-level accounting responsibilities:

Accountants can expect to take on the following responsibilities in their first accounting job out of college.

Note: These often overlap with junior accountant job responsibility, as the positions are interchangeable at most firms.

- Keeping and recording financial transactions

- Preparing financial reports such as balance sheets and income statements

- Updating accounts payable and sending invoices

- Assisting mid-level and staff accountants

Mid-level accounting jobs can eventually transition into other positions after working with an organization for several years. Knowing what to expect from these positions allows them to develop their skills and focus on essential areas of study so they’ll be well-suited for the role after gaining enough experience.

Mid-Level accounting job responsibilities

After gaining a few years of experience, an accountant may be trusted with the following additional responsibilities. A bachelor’s degree is usually required for a mid-level accounting position as well.

Note: These responsibilities often overlap with staff accountant job responsibility, as the titles are interchangeable at most firms.

- Supervise accounts payable and accounts receivable

- Supervise payroll

- Work with the management team to analyze competitors

- Create detailed financial plans

- Prepare annual reports

- Prepare taxes and work to achieve the highest refund possible for the organization

What do you think?

Is there an area of accounting you would most like to pursue?

Additional Resources for Accountant Job Duties

CPA

Upon entering their undergraduate program, many students find themselves asking, “What does a CPA do?” Although it’s one of the most common accounting jobs, there’s a surprising amount of confusion surrounding the title. Students must understand the difference between a CPA and a regular accountant before settling on a career path.

While five states allow accountants to become CPAs without an accounting degree, the vast majority require a bachelor’s degree or 150 credit hours in accounting before students can sit for the CPA exam. The CPA exam is notoriously difficult, and many students are intimidated because they’ve heard that 50% of test-takers fail on their first attempt. You can take the exam as many times as you need to pass (but only once per testing window). If you’re pursuing a bachelor’s in accounting, you’ll spend plenty of time preparing for the exam during all your undergraduate courses.

After earning their license, CPAs have some unique abilities that other accountants don’t have. They’re permitted to prepare audited and reviewed financial statements, while other accountants can only prepare compiled statements. Since public companies must produce audited statements to comply with regulations, CPAs are in greater demand than other accountants. As a result, they can expect to earn an average of 15% more income as well.

What do you think?

Are you considering a career as a CPA?

Additional Resources for CPA

Section 10: Typical Courses Accounting Students Take

The following courses are included in many accounting programs across the country. A brief overview of the curriculum will let students know what to expect when it comes time to take the class.

- Financial Accounting: At many schools, this course is also called “Accounting 101.” Students learn all the fundamentals of the business and gain an understanding of key principles such as GAAP and technology in accounting. They also learn about proper business ethics.

- Managerial Accounting: This course will teach students the differences between managerial accounting and financial accounting. They’ll learn key terms, problem- solving techniques, and more. Budget preparation and planning will be discussed as well, and students will learn how to coordinate with a business management team to boost profits.

- Accounting Software and Information Systems: This course teaches students to prepare financial statements, budgets, and special reports using accounting software. Students will become familiar with the software most commonly used at businesses across the country.

- Foundations of Business: This course teaches students how to use strategic thinking to apply business theory to their accounting position. Students will learn how to make informed decisions by conducting financial analyses as well.

- Creativity, Innovation and Entrepreneurial Thinking: This course stresses the importance of thinking creatively in a business setting. Strategies for forming an entrepreneurial mindset are also discussed.

- Introduction to Computational Thinking for Business: Students will learn to solve problems using data analysis based on a computational model. They’ll study algorithms, automation, and other key concepts

Additional Resources for Accounting Courses

Section 11: List of Accounting Degrees (and Descriptions)

Some students may have questions about the different accounting degrees and specializations available to them. Here are the most common degrees most accounting students pursue, as well as the specializations they choose to accompany them.

- Associate’s in Accounting: A two-year degree that qualifies the recipient for entry-level accounting jobs such as accounts payable clerk, payroll clerk, and bookkeeper.

- Bachelor’s in Accounting: A four-year degree that allows graduates to take on mid-level accounting jobs such as auditor and financial planner. It is also part of the qualification process for becoming a CPA.

- Master’s in Accounting: An advanced degree that qualifies the recipient for high-paying jobs such as CFO, corporate accountant, and management positions.

- MBA in Accounting: An advanced degree like a Master’s in Accounting that allows the recipient to fill high-level accounting positions such as financial advisor and manager.

- PhD or DBA in Accounting: The highest-level accounting degrees. These will qualify the recipient for the most advanced accounting jobs. Recipients will also be able to teach as a university professor.

Specializations:

- Accounting and Business Management: A specialization that prepares students for a high-level accounting job working with managerial teams. The business side of accounting is heavily emphasized.

- Financial Accounting: A specialization that deals with preparing financial reports for business and public use. Students who choose this path will become exports in reporting.

- Forensic Accounting: This specialization prepares students to study financial crimes and to analyze evidence in criminal cases.

Taxation Accounting: This specialization prepares students to deal directly with the IRS and helps them become experts at preparing taxes.

Additional Resources for Accounting Degrees

- 20 Best Online Associates in Accounting Degree Programs

- 20 Best Online Bachelor’s in Accounting Degree Programs

Other Courses:

- Introduction to Philosophy

- Introduction to Business Administration

- Introduction to Entrepreneurship

- Introduction to Finance

- Introduction to Economics

- Introduction to Investing

- Introduction to Nutrition

- Introduction to Interior Design

- Introduction to Digital Marketing

- Introduction to Real Estate

- Introduction to Hospitality Management